Global Broker Regulation Inquiry App

About WikiFX

English

简体中文

繁體中文

English

Pусский

日本語

ภาษาไทย

Tiếng Việt

Bahasa Indonesia

Español

हिन्दी

Filippiiniläinen

Français

Deutsch

Português

Türkçe

한국어

العربية

اردو

ETO Markets TrendWatch|Mag 7 Earnings Split Widens as Markets Test AI Delivery

Abstract:Since late April, earnings from the US “Magnificent Seven” have arrived in rapid succession, and the markets pricing logic is undergoing a structural shift. Over the past two years, investors were wil

Since late April, earnings from the US “Magnificent Seven” have arrived in rapid succession, and the markets pricing logic is undergoing a structural shift. Over the past two years, investors were willing to pay for the AI narrative itself. Entering 2026, capital markets now evaluate three questions:

Whose AI demand is real?

Whose cash flow is durable?

Whose capital expenditure can convert into real profit?

Nvidia: Compute Anchor Awaiting New Results

Nvidia has not yet released results for the quarter ending April 26 and will report on May 20. Markets continue to trade on its previous quarter: revenue of 68.13 billion dollars, data center revenue of 62.3 billion dollars, net profit of 42.96 billion dollars and a gross margin of 75 percent. Guidance for the upcoming quarter is 78 billion dollars, excluding all China related data center revenue.

Nvidia remains the most certain beneficiary of the AI compute cycle. Yet investor focus has shifted from profit scale to the production timeline of Blackwell products and whether growth momentum can hold after removing China related demand.

Microsoft: The Most Stable Enterprise Beneficiary

Microsoft reported revenue of 82.9 billion dollars for the quarter ending March 31, up 18 percent, with net profit up 23 percent. Cloud revenue reached 54.5 billion dollars, up 29 percent, and Azure grew 40 percent. Management disclosed that AI related annualized revenue has surpassed 37 billion dollars.

Microsofts advantage lies in the combined strength of cloud cash flow, AI driven incremental demand and high enterprise software stickiness. AI is no longer conceptual but embedded into cloud growth and enterprise procurement, forming a complete commercial loop that supports sustained cash flow.

Alphabet: Cloud Growth Accelerates

Alphabet reported revenue of 109.896 billion dollars, up 22 percent, with operating profit rising to 39.696 billion dollars. Google Cloud revenue grew 63 percent to 20.028 billion dollars, with operating profit rising sharply. The company also recorded 37.716 billion dollars of unrealized investment gains, lifting net profit to 62.578 billion dollars.

The key revaluation driver is Google Cloud entering a high growth, high profitability phase. However, part of the profit surge comes from investment gains rather than core operations. Alphabets valuation now reflects a dual structure: long term value anchored by search and cloud fundamentals, and short term sentiment driven by investment volatility.

Meta: Market Questions Rising Capital Expenditure

Meta reported revenue of 56.311 billion dollars, up 33 percent, with operating profit of 22.872 billion dollars. Net profit reached 26.773 billion dollars, partly boosted by 8.03 billion dollars in tax benefits. Capital expenditure reached 19.84 billion dollars, and full year guidance was raised to as high as 145 billion dollars.

Meta shows a clear split: advertising continues to generate strong cash flow, while AI infrastructure requires heavy investment. The core question is whether profit growth can keep pace with rising costs.

Amazon: AWS Returns to High Growth

Amazon reported revenue of 181.5 billion dollars, up 17 percent. AWS revenue grew 28 percent to 37.6 billion dollars. Net profit reached 30.3 billion dollars, including 16.8 billion dollars of gains from its Anthropic investment. Operating cash flow rose to 148.5 billion dollars, but free cash flow remained low due to heavy AI related investment.

AWS returning to strong growth is the core highlight. Amazon faces the balance between core business cash generation and AI investment, but its diversified cash flow across e commerce, advertising, cloud and custom chips provides stronger resilience.

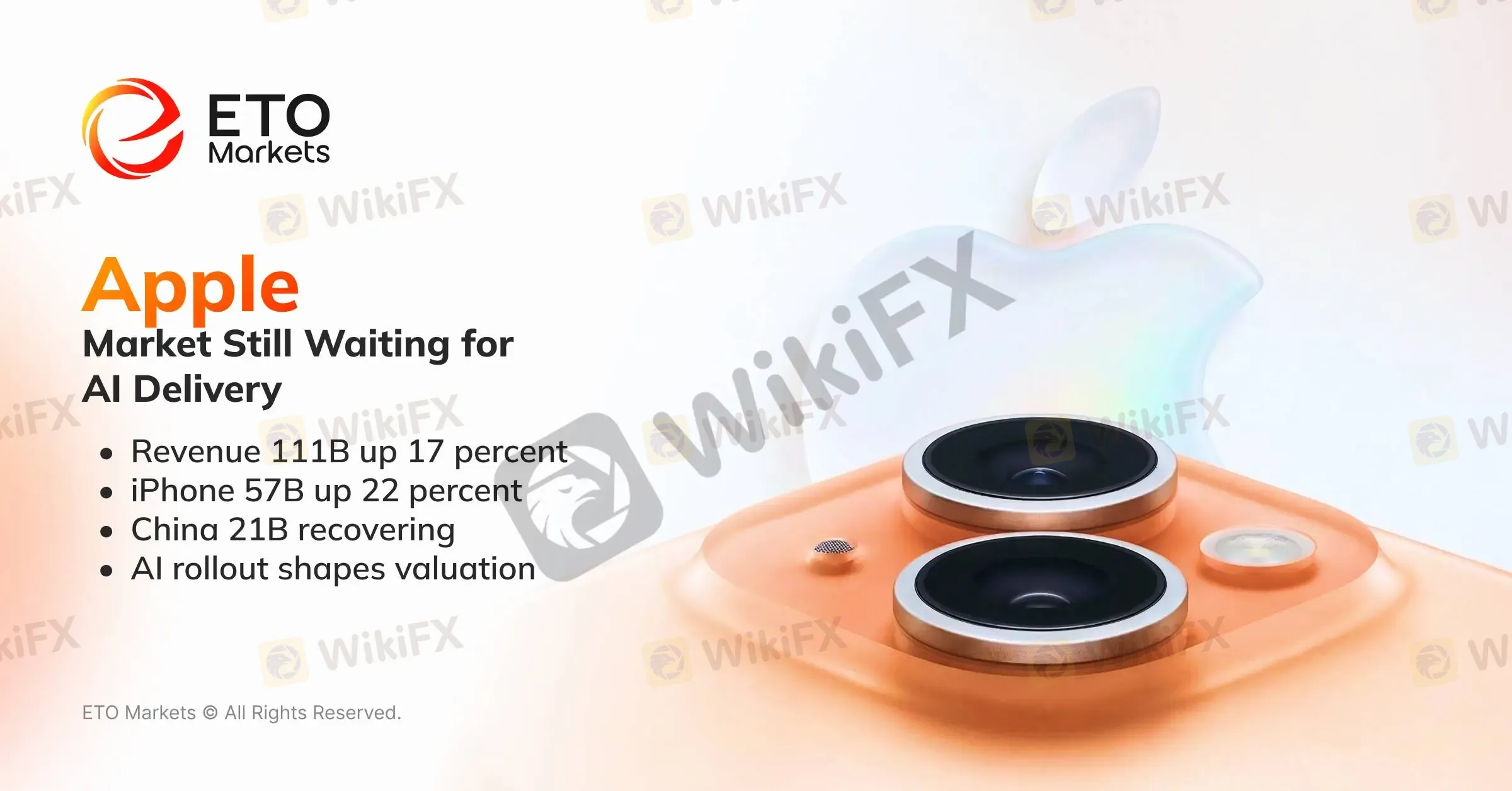

Apple: Market Still Waiting for AI Delivery

Apple reported revenue of 111.2 billion dollars for the quarter ending March 28, up 17 percent, with EPS up 22 percent. iPhone revenue grew 22 percent, services hit a new high and Greater China revenue rebounded to 20.5 billion dollars.

Apples challenge is not profitability but the slow pace of new AI driven growth. Hardware demand remains solid and services continue to expand, but market expectations have shifted toward the commercial rollout of Apple Intelligence.

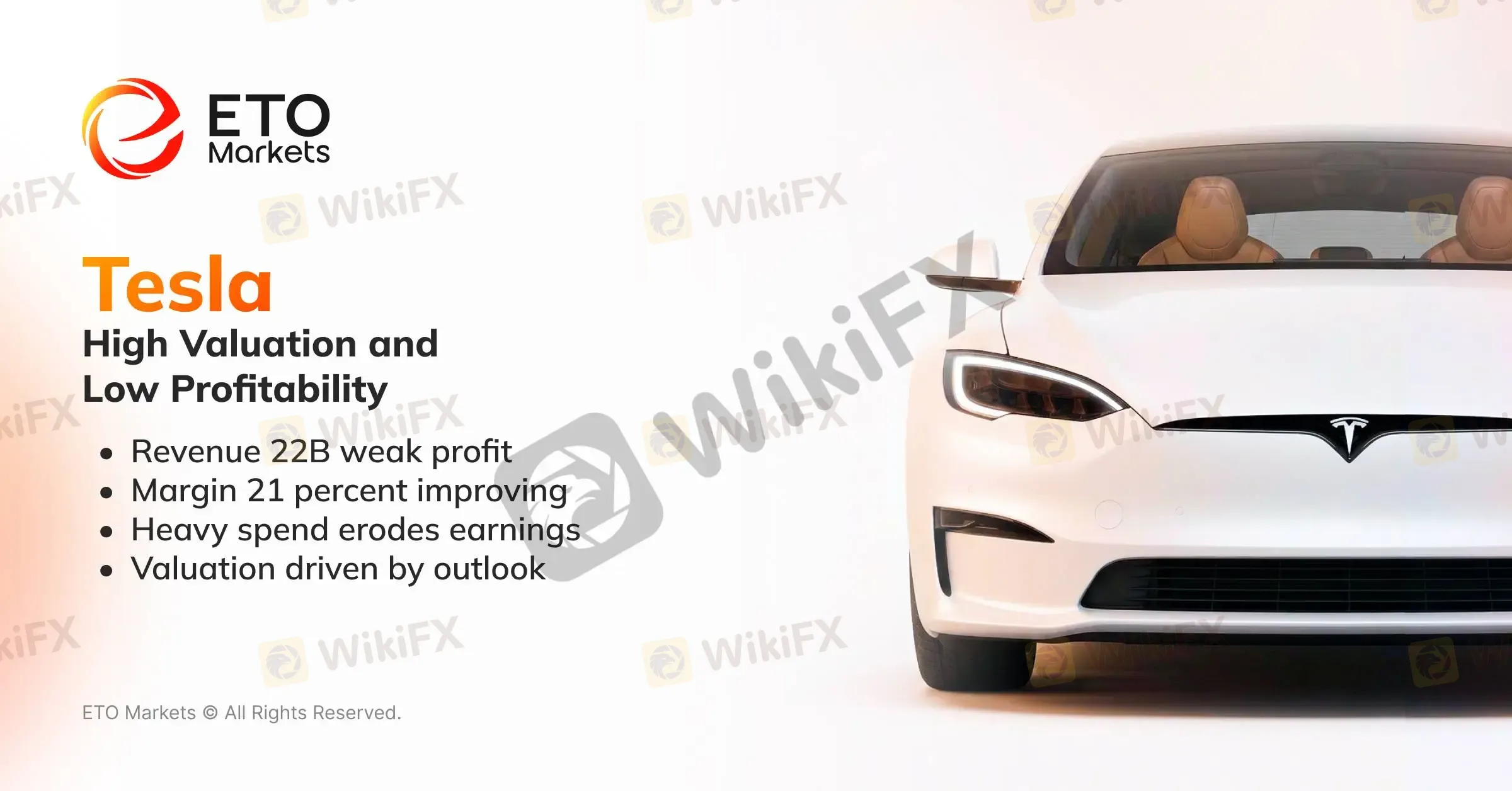

Tesla: High Valuation and Low Profitability

Tesla reported revenue of 22.387 billion dollars and net profit of only 477 million dollars. Automotive gross margin improved to 21.1 percent, signaling easing price pressure. However, profitability remains weak due to heavy investment in autonomous driving, robotics and compute infrastructure.

Tesla still receives valuation premium for long term innovation, but among major tech names it has the weakest current profitability and the highest reliance on future expectations.

Disclaimer:

The views in this article only represent the author's personal views, and do not constitute investment advice on this platform. This platform does not guarantee the accuracy, completeness and timeliness of the information in the article, and will not be liable for any loss caused by the use of or reliance on the information in the article.

WikiFX Broker

Latest News

Singapore tightens monetary policy in surprise move as rising oil prices rekindle inflation risk

WikiFX

WikiFXSPREDIX MARKETS Review: What Traders Should Know Before Depositing

WikiFXBXB Review – Zero Regulation, Dead Website: What Traders Need to Know

WikiFXHFM Review: No Regulatory Licences and a 1.83 Score , Is Your Deposit Safe?

WikiFXIs Your Withdrawal Plan Killing Your Compounding Gains?

WikiFXHFMARKETS TRADE Review: Zero Regulation and a Central Bank Warning

WikiFXWinvest Review: What Traders Should Know Before Depositing

WikiFXTrade Nation Review: What Traders Should Know Before Depositing

WikiFXFXPesa Review: Is Your Deposit Safe?

WikiFXXM Royal Scam Drains RM119,599 From Malaysian Housewife

WikiFX